The Bank Of Canada just raised rates by a massive 100 basis points. This follows multiple other successive rate increases, commencing shortly after peak market conditions in February of 2022. This July 13th increase, by most popular consensus, will not be the last either. There is expected to be further increases. There is very little doubt that this will further shift the market towards a more buyer friendly market, if not a full blown buyers market. However, this leads us to ask; which buyers are best situated to buy in this high interest market? If indeed it is a buyers market, should buyers step in? Is it time to act? First let us establish the current state of the market.

The criteria for a buyers market is composed of four major elements;

An excess of supply relative to low demand

Lower Sales To Listings Ratio

Longer Days On Market

Lower Prices

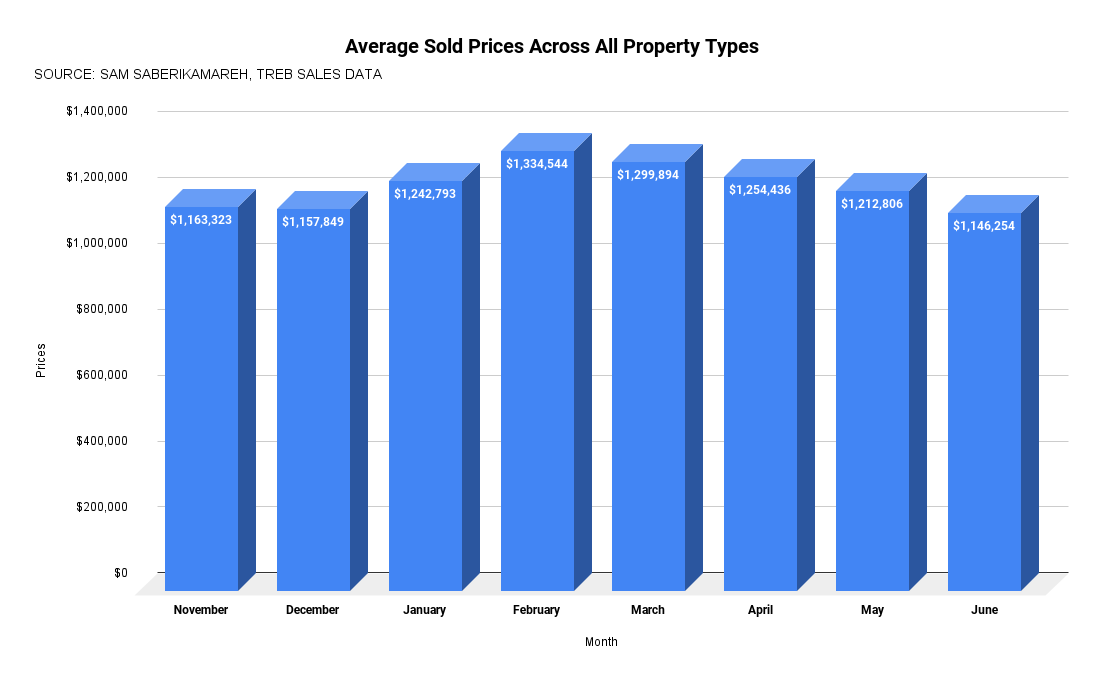

When we take a look at the Toronto and GTA Real Estate Market, one can clearly see these four signs illustrated. As of June 2022, there were about 16,347 new listings in terms of supply, yet demand was far less impressive. Less buyers involved in the market, less offers, less mortgage pre-approvals and less showings. Of these 16,347 new listings, only 6,474 thousand managed to sell! This further shows us a very low sales to listings ratio. The average home available for sale in the Greater Toronto Area sat on the market for about 24 days, which represents a 7 day from the year before. Lastly, although prices are still up year over year for all areas, they are down from the peak market conditions in February, as we see from the chart below.

Prices have fallen from $1,334,544 in February of 2022 down to $1,146,254 across the GTA, when we take a look at all property types. Yet these conditions; the lower prices, the lower demand, lower sale volume and longer availability for properties – owe their cause to the very same conditions that makes it difficult for buyers to take advantage; high interest rates!

The rate hikes by the Bank Of Canada effectively eliminate some of the buyers borrowing ability, while others have their borrowing capacity greatly reduced. The former are completely removed from the market, whereas the latter see their options are reduced to varying, yet noticeable, degrees. When demand diminishes in such a fashion, and supply does not slow down, this creates the very conditions we have discussed.

As the result of the impact of increased rates on both buyers and sellers, the buyers who are best positioned to take advantage of this market are cash buyers. Those buyers who are purchasing with 50% to 100% down. Without a doubt, it is time for these highly liquid buyers to take advantage. This certainly does not mean that there is a rush. This means that these buyers are prone to the fragility of most other buyers who require financing. These cash or mostly cash buyers get to enjoy the benefits of a buyers market without being impacted by the cause of it. In other words put; they get to take advantage of, for example, the discounted prices of homes without being impacted by the high borrowing rates that caused the discounted prices in the first place. For these cash buyers, it is nearly all upside and very little opportunity cost. There certainly should be no rush to buy, as further rate hikes are coming; however cash buyers face very optimistic prospects in the coming months and rest of 2022.

In conclusion, the increase in interest rates has made the Toronto and Greater Toronto real estate market very buyer friendly. Yet, a lot of buyers with low down payments are not able to take advantage of these friendly market conditions for the very reason the market conditions exist in the first place; high rates. Prices may come down as rates go up, but borrowing power drops in unison for a lot of regular home buyers. Consequently, the buyers who are best able to take advantage of this soft market are those who are highly liquid, and should consider their purchasing prospects with ease and patience for months to come.

Not intended to be financial or legal counsel, and based upon the professional opinion of Mehran Malekzadeh